Argentina's first unified banking wallet: From zero to 3 million users

INDUSTRY

Fintech

YEAR

2020-2021

PLATFORM

iOS and Android

What I did

I joined MODO a few months before launch as one of the founding product designers. Early on, I helped define core flows, and after launch, I owned the peer-to-peer transfer experience, one of only two products available to users in the first six months.

I joined MODO a few months before launch as one of the founding product designers. Early on, I helped define core flows, and after launch, I owned the peer-to-peer transfer experience, one of only two products available to users in the first six months.

3M

3M

users in the

fist 10 months

30+

30+

banks in

the ecosystem

400K+

400K+

merchants

locations

nationwide

Read Case Study

In the first six months after launch:

Tripled the number of active P2P users

Increased x3 the transfers executed

Reduced the error rate by 30 percentage points

Improved account linking conversion by 15 percentage points

Integrated 10 new banks into the P2P flow

Shipped suggested contacts, personal QR code, and push notifications for received money

In the first six months after launch:

Tripled the number of active P2P users

Increased x3 the transfers executed

Reduced the error rate by 30 percentage points

Improved account linking conversion by 15 percentage points

Integrated 10 new banks into the P2P flow

Shipped suggested contacts, personal QR code, and push notifications for received money

A system that shaped the brand

Weeks before launch, we worked with a creative agency under a tight deadline to redesign the UI — stripping it back to something more minimal and intentional. A set of custom illustrations helped define the tone: warm, approachable, and a little playful.

The swipe gesture used to send money and pay became the product's signature interaction — and the illustrations reinforced it, giving the motion a personality that felt distinctly MODO.

Weeks before launch, we worked with a creative agency under a tight deadline to redesign the UI — stripping it back to something more minimal and intentional. A set of custom illustrations helped define the tone: warm, approachable, and a little playful.

The swipe gesture used to send money and pay became the product's signature interaction — and the illustrations reinforced it, giving the motion a personality that felt distinctly MODO.

Sending money, without the friction

Sending money in MODO only required one thing: the other person's phone number, no bank account details, no extra steps. If they were nearby, a personal QR code made it even faster, both options weren't common in Argentine banking apps at the time. Over time, we iterated on the flow adding features like suggested contacts, filters, and push notifications for received money, each one coming from real friction we observed in how people used it.

Sending money in MODO only required one thing: the other person's phone number, no bank account details, no extra steps. If they were nearby, a personal QR code made it even faster, both options weren't common in Argentine banking apps at the time. Over time, we iterated on the flow adding features like suggested contacts, filters, and push notifications for received money, each one coming from real friction we observed in how people used it.

Associate your bank accounts

Associate your bank accounts

Associate your bank accounts

Send money between accounts

Send money between accounts

Send money between accounts

Send money between accounts

Push notifications

Push notifications

Push notifications

Send and receive money using a personal QR Code

Send and receive money using a personal QR Code

Send and receive money using a personal QR Code

Request money, the other side of the transaction

This flow was thought with situations in mind like splitting the cost after a tennis match, chipping in for a group gift, or settling up after dinner — where nobody wants to chase people or remember exact amounts. The request flow handled that context by letting the sender set the amount and reason, so the other person just had to confirm.

This flow was thought with situations in mind like splitting the cost after a tennis match, chipping in for a group gift, or settling up after dinner — where nobody wants to chase people or remember exact amounts. The request flow handled that context by letting the sender set the amount and reason, so the other person just had to confirm.

Contributing to merchant payments

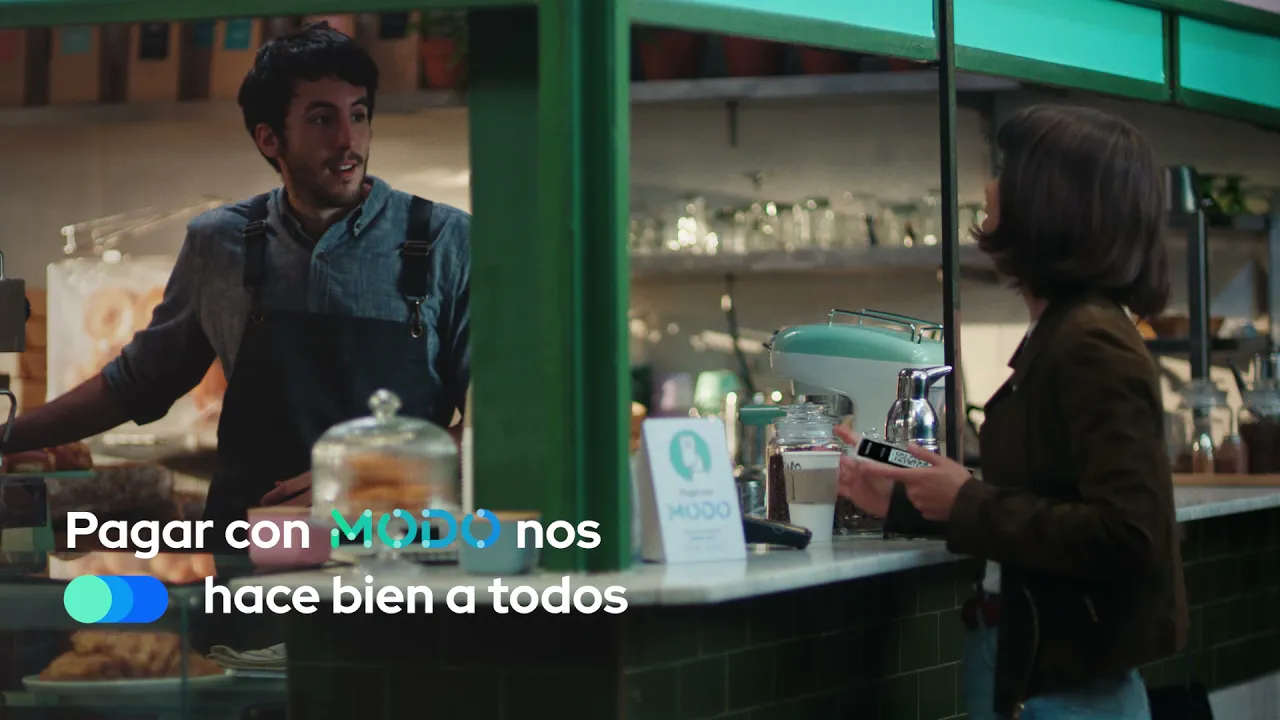

Pay was a collaborative effort, I wasn't the sole owner here, but I contributed to key design decisions around the merchant-facing flow and influenced how we communicated payment confirmation to users. Acceptance at 400K+ merchant locations nationwide meant the interaction had to work across very different contexts: small vendors, large retailers, and everything in between.

Pay was a collaborative effort, I wasn't the sole owner here, but I contributed to key design decisions around the merchant-facing flow and influenced how we communicated payment confirmation to users. Acceptance at 400K+ merchant locations nationwide meant the interaction had to work across very different contexts: small vendors, large retailers, and everything in between.

Project details

Team

Three product designers (including me), one UXR, one Head of UX

Duration

~18 months, from 2020 to 2021

My Role

Founding Product Designer — owned P2P transfers end-to-end, contributed to P2M and acquisition flows

What I did

I joined MODO a few months before launch as one of the founding product designers. Early on, I helped define core flows, and after launch, I owned the peer-to-peer transfer experience, one of only two products available to users in the first six months.

3M

users in the

fist 10 months

30+

banks in

the ecosystem

400K+

merchants

locations

nationwide

Read Case Study

In the first six months after launch:

Tripled the number of active P2P users

Increased x3 the transfers executed

Reduced the error rate by 30 percentage points

Improved account linking conversion by 15 percentage points

Integrated 10 new banks into the P2P flow

Shipped suggested contacts, personal QR code, and push notifications for received money

A system that shaped the brand

Weeks before launch, we worked with a creative agency under a tight deadline to redesign the UI — stripping it back to something more minimal and intentional. A set of custom illustrations helped define the tone: warm, approachable, and a little playful.

The swipe gesture used to send money and pay became the product's signature interaction — and the illustrations reinforced it, giving the motion a personality that felt distinctly MODO.

Sending money, without the friction

Sending money in MODO only required one thing: the other person's phone number, no bank account details, no extra steps. If they were nearby, a personal QR code made it even faster, both options weren't common in Argentine banking apps at the time. Over time, we iterated on the flow adding features like suggested contacts, filters, and push notifications for received money, each one coming from real friction we observed in how people used it.

Associate your bank accounts

Send money between accounts

Push notifications

Send and receive money using a personal QR Code

Request money, the other side of the transaction

This flow was thought with situations in mind like splitting the cost after a tennis match, chipping in for a group gift, or settling up after dinner — where nobody wants to chase people or remember exact amounts. The request flow handled that context by letting the sender set the amount and reason, so the other person just had to confirm.

Contributing to merchant payments

Pay was a collaborative effort, I wasn't the sole owner here, but I contributed to key design decisions around the merchant-facing flow and influenced how we communicated payment confirmation to users. Acceptance at 400K+ merchant locations nationwide meant the interaction had to work across very different contexts: small vendors, large retailers, and everything in between.

Project details

Team

Three product designers (including me), one UXR, one Head of UX

Duration

~18 months, from 2020 to 2021

My Role

Founding Product Designer — owned P2P transfers end-to-end, contributed to P2M and acquisition flows