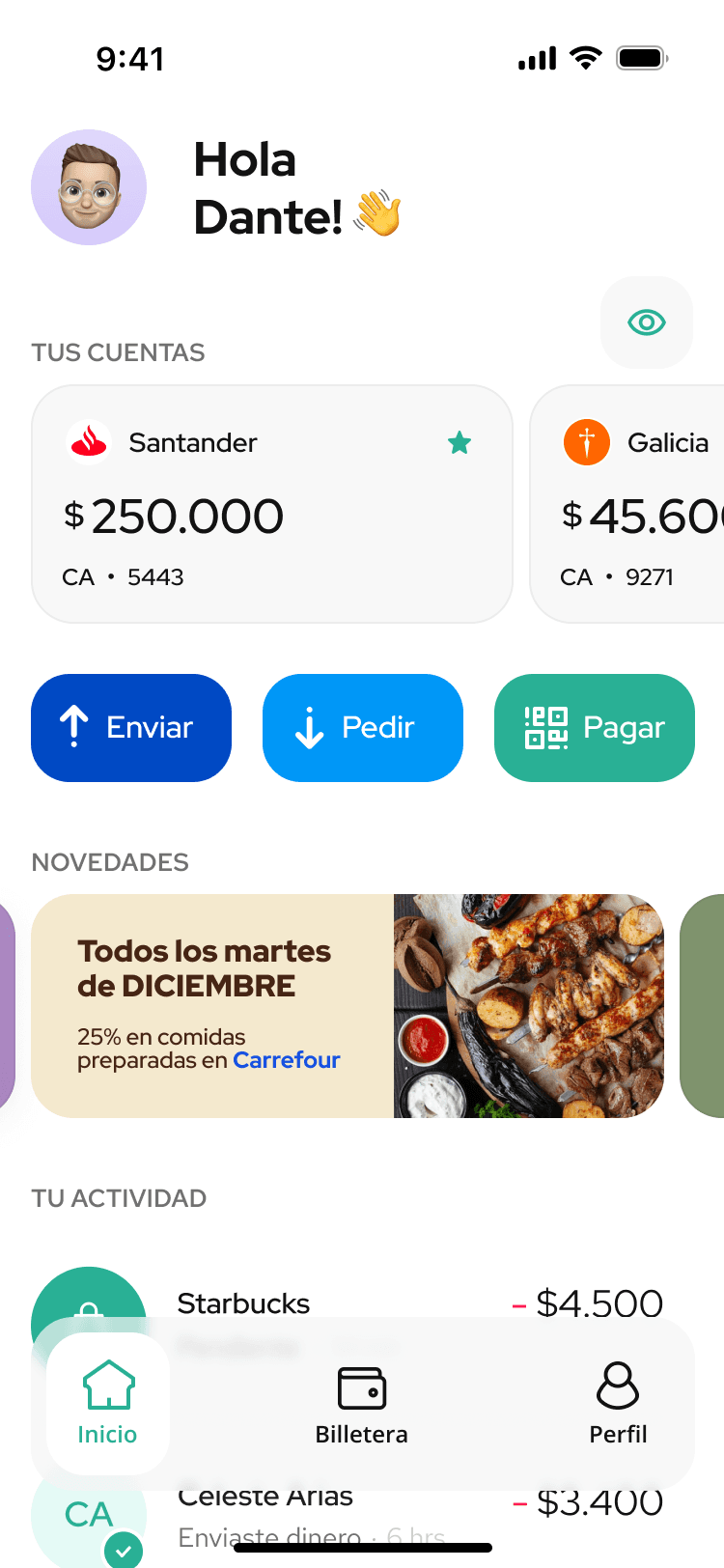

MODO

Argentina's first unified banking wallet, from zero to 3 million users

My Role

I joined as a Senior Product Designer and I owned the P2P (peer-to-peer) experience, also known as money transfers. During the first six months, P2P was one of only two pillars of the app. Also, I contributed to acquisition flows, merchant payments, account linking, and the design system. I run usability tests and interviews. I worked with data engineers to track user behavior, and I wrote guidelines for the 30+ banking apps that integrated MODO's features.

The Challenge

I contributed to remove the friction, create an habit and ease of use delivering features such as: Suggested contacts, personal QR code, push notifications, push provisioning to be available not only on the independent app, but also the banking apps.

Project Details

Timeline: 2020-2021 (~14 months) // Platform: iOS and Android // P2P Team: Myself (Senior Product Designer), Sofia Alric (Senior Product Manager), Pablo Battro (Associate Product Manager), Ignacio Reyna (Data Engineer)

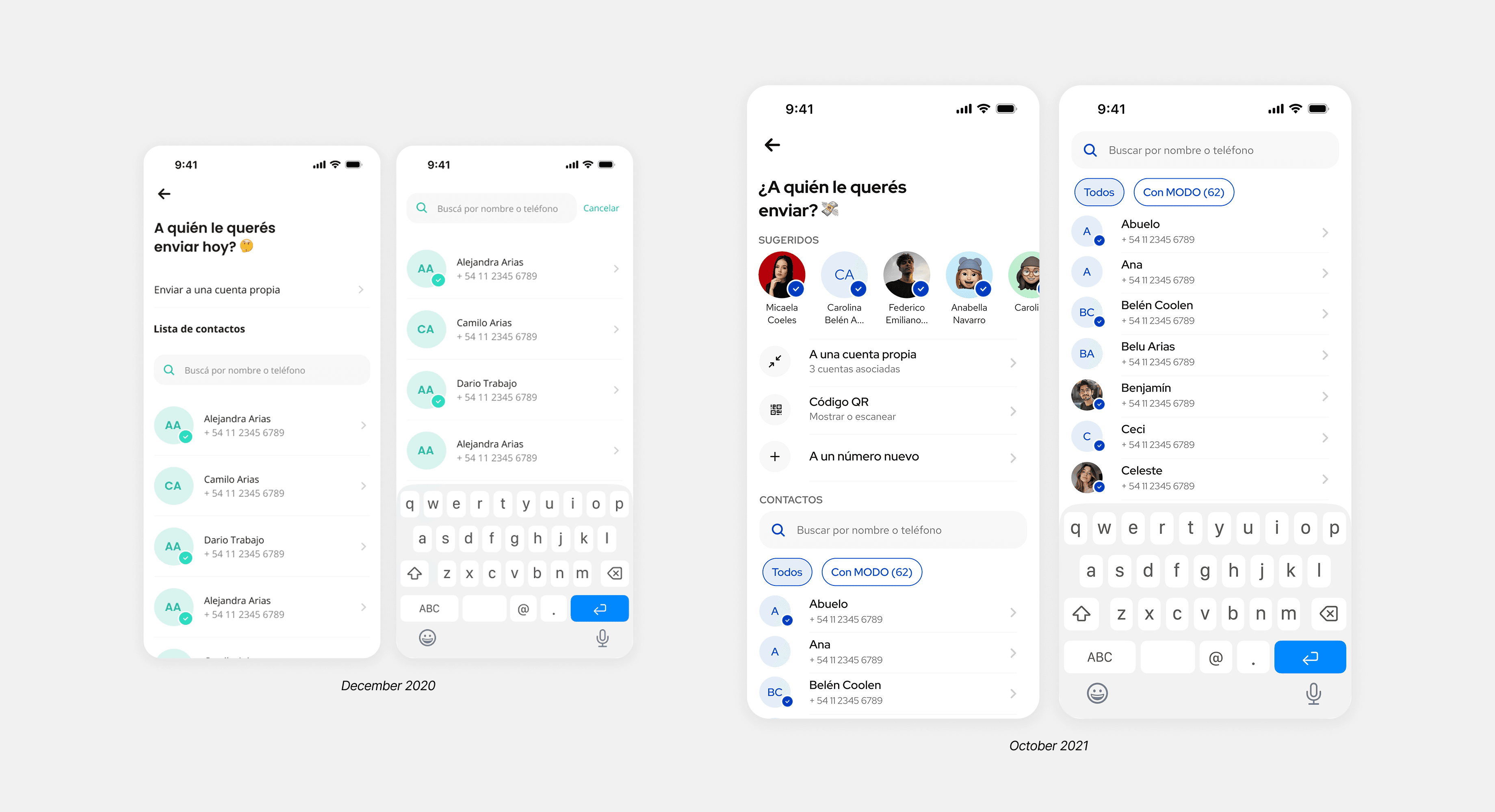

Contacts screen iteration in 10 months.

Features and improvements launched

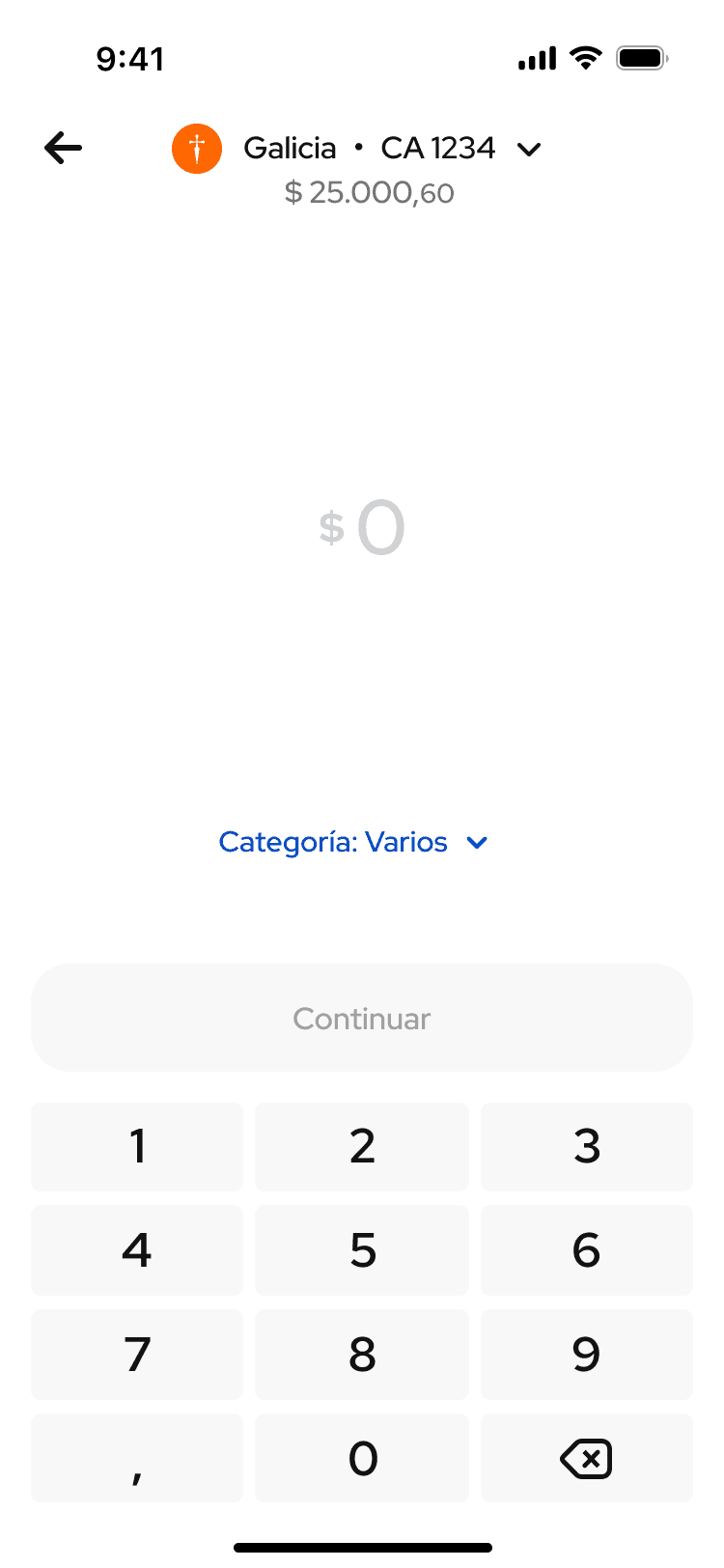

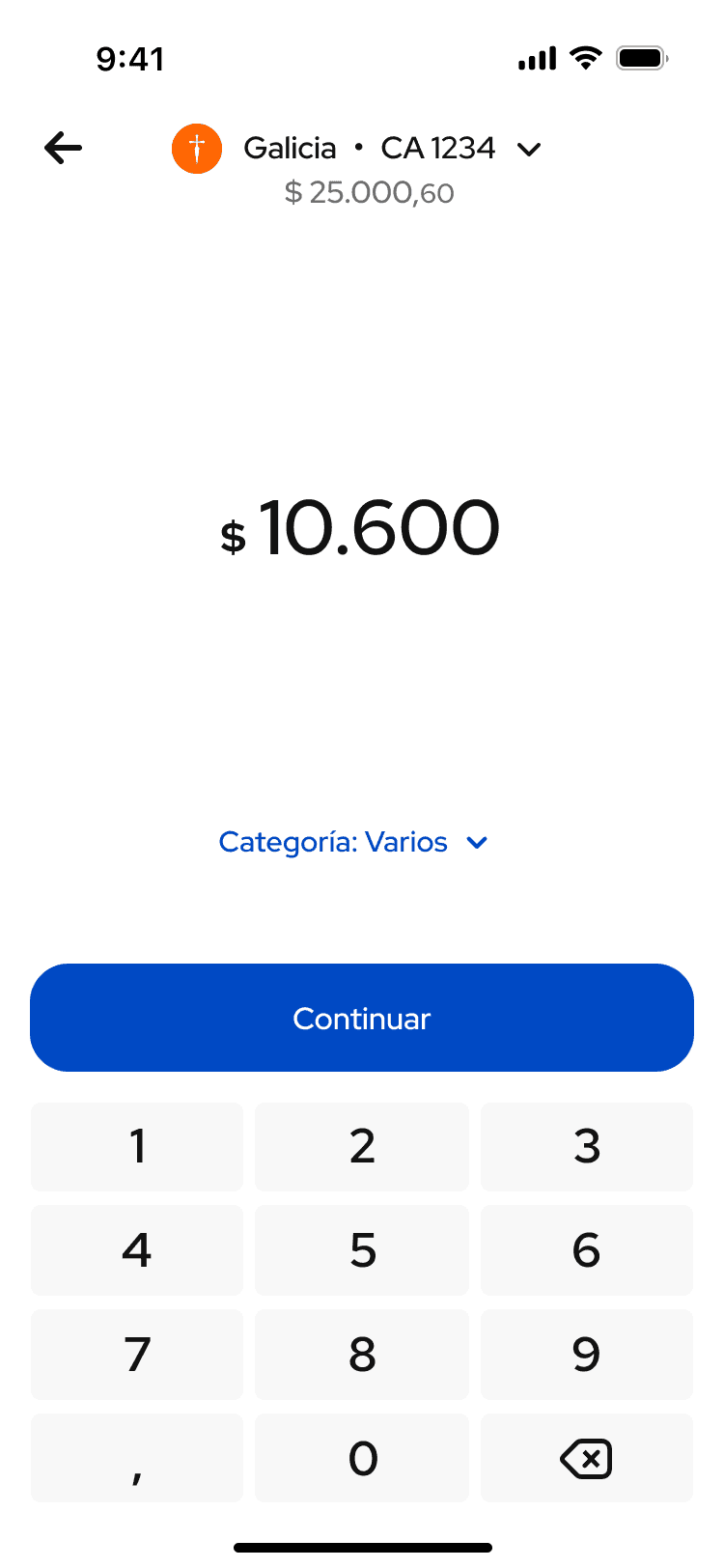

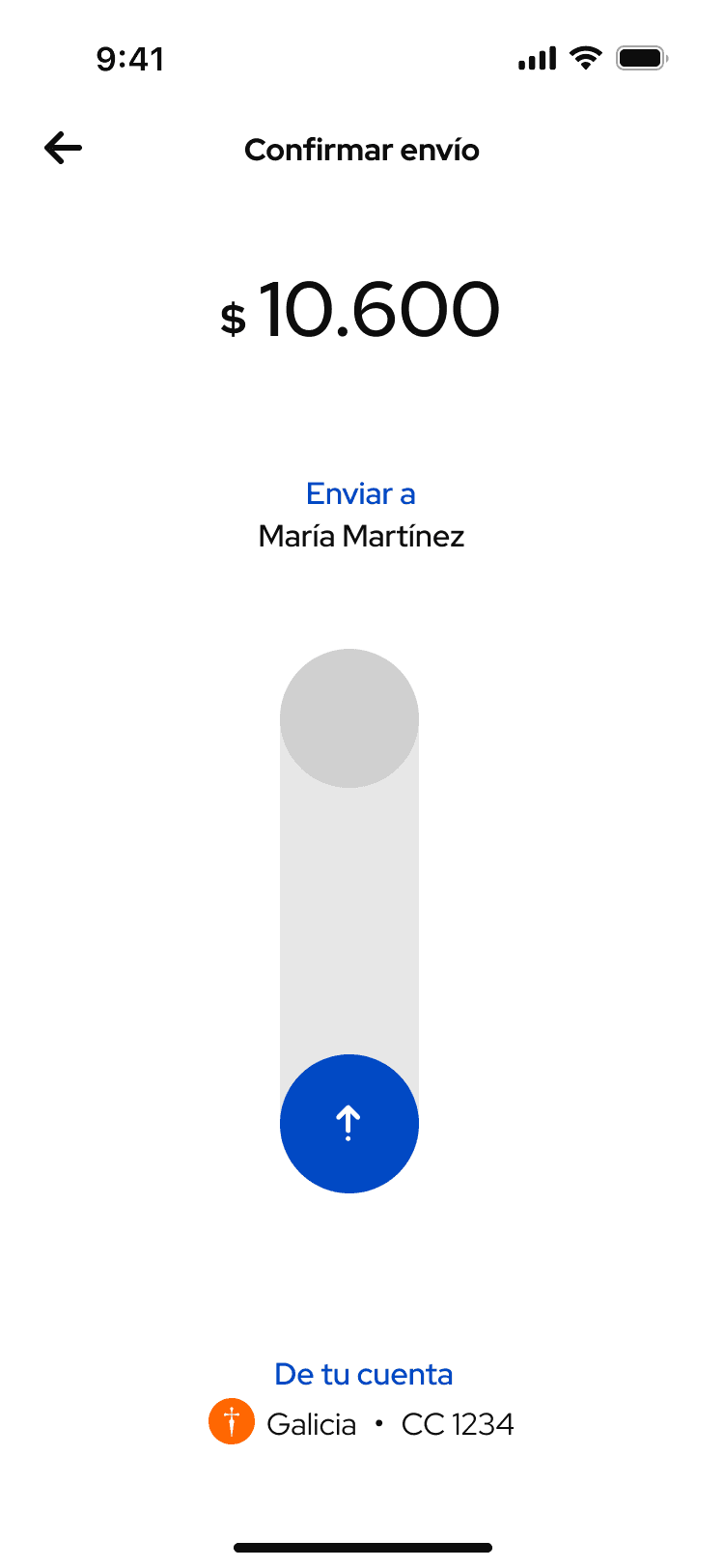

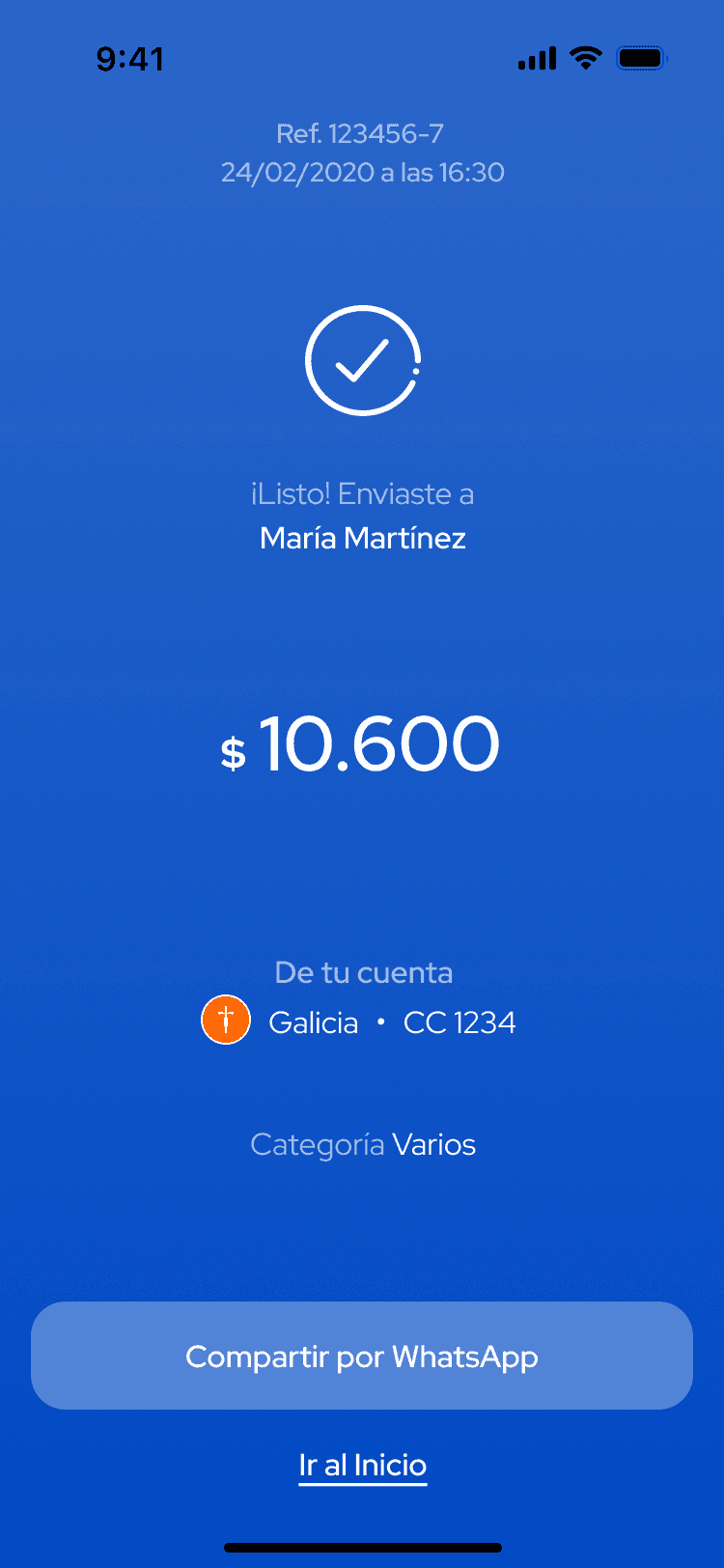

Payment Slider

Confirmation

Problem

How do you confirm a payment in a way that feels intentional and still differentiates MODO from every other banking app?

What we did

We designed a vertical swipe-up gesture instead of the standard tap-to-confirm button. The interaction included micro animations, sound, and haptic feedback to make the moment feel real, not just functional. It also made accidental confirmations nearly impossible.

The swipe became central to MODO's identity and differentiate it from other competitors at that time.

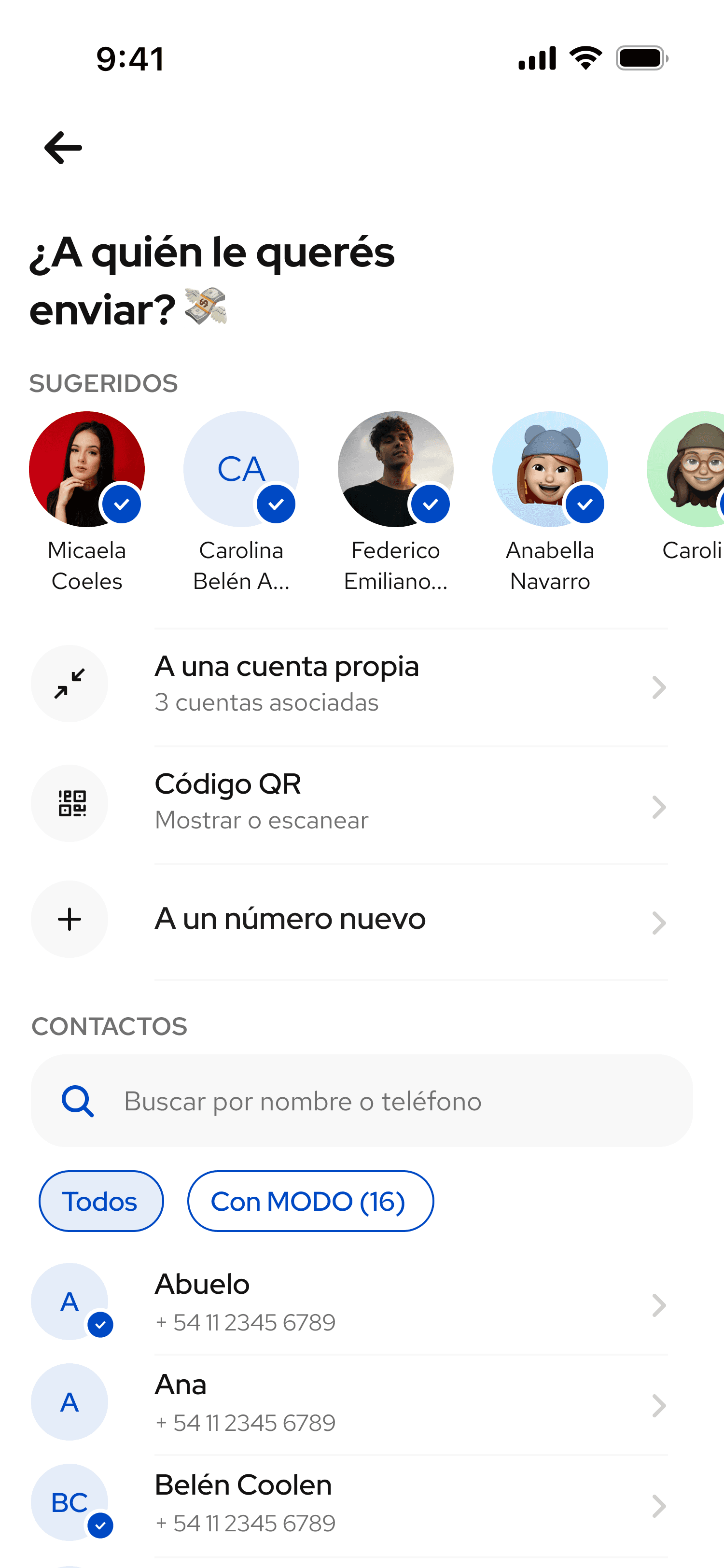

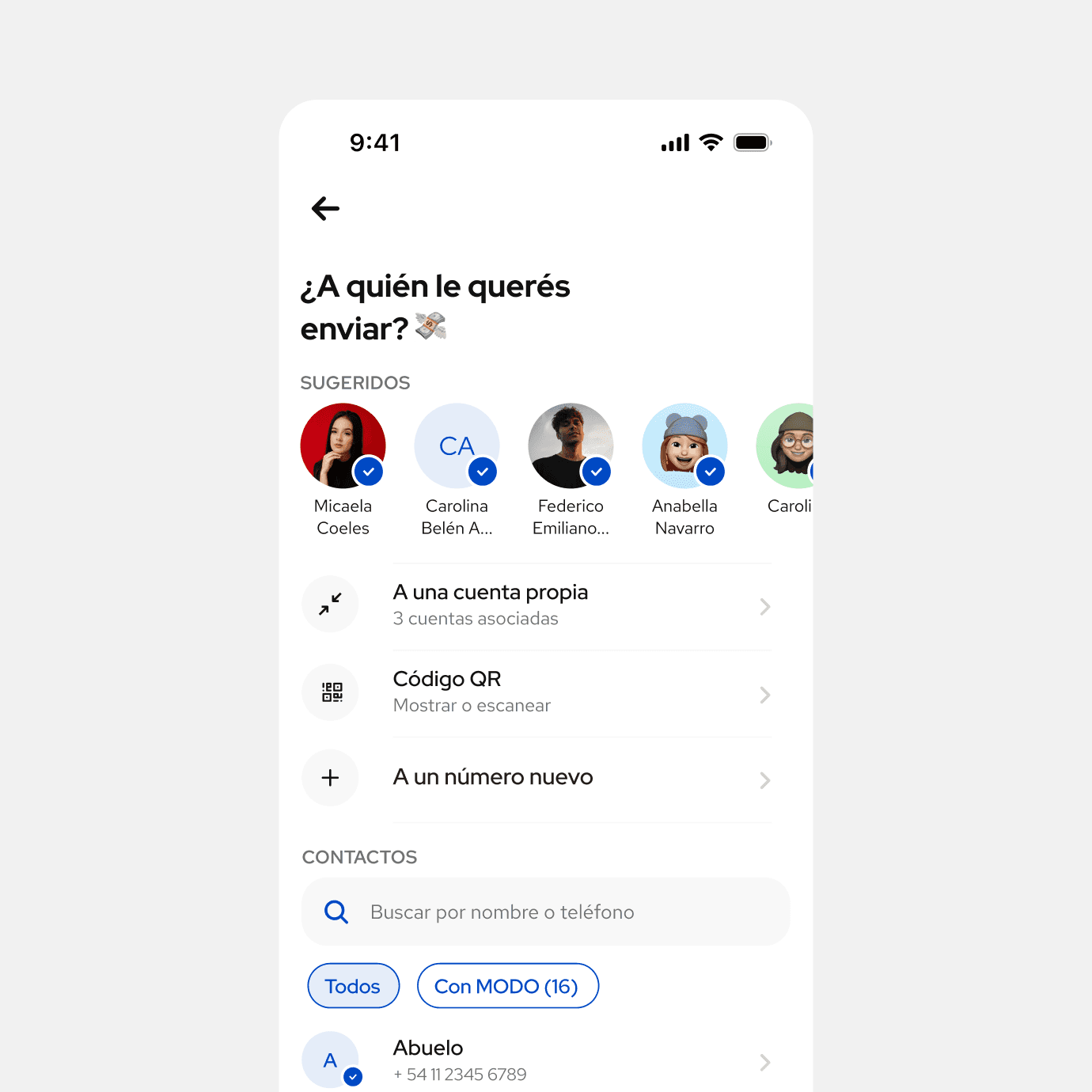

Suggested Contacts

Problem

Even with a search bar, finding someone to send money to required real mental effort. You had to think of a name, type it, and scan results, every time.

What we did

We added a row of suggested contacts at the top of the screen — people the user had already transacted with across the MODO ecosystem, no matter which banking app they used.

Result

Users with suggested contacts completed transfers about 30% faster.

Additional notes

Early on, we also added a filter showing which contacts already had MODO. This mattered because tapping on someone without MODO would leave the transfer pending. Showing it upfront set the right expectation.

We considered most frequent or most recent, but we didn't have reliable data yet. We went with contacts who had consistent transaction history using MODO, a trade off between personalization and accuracy.

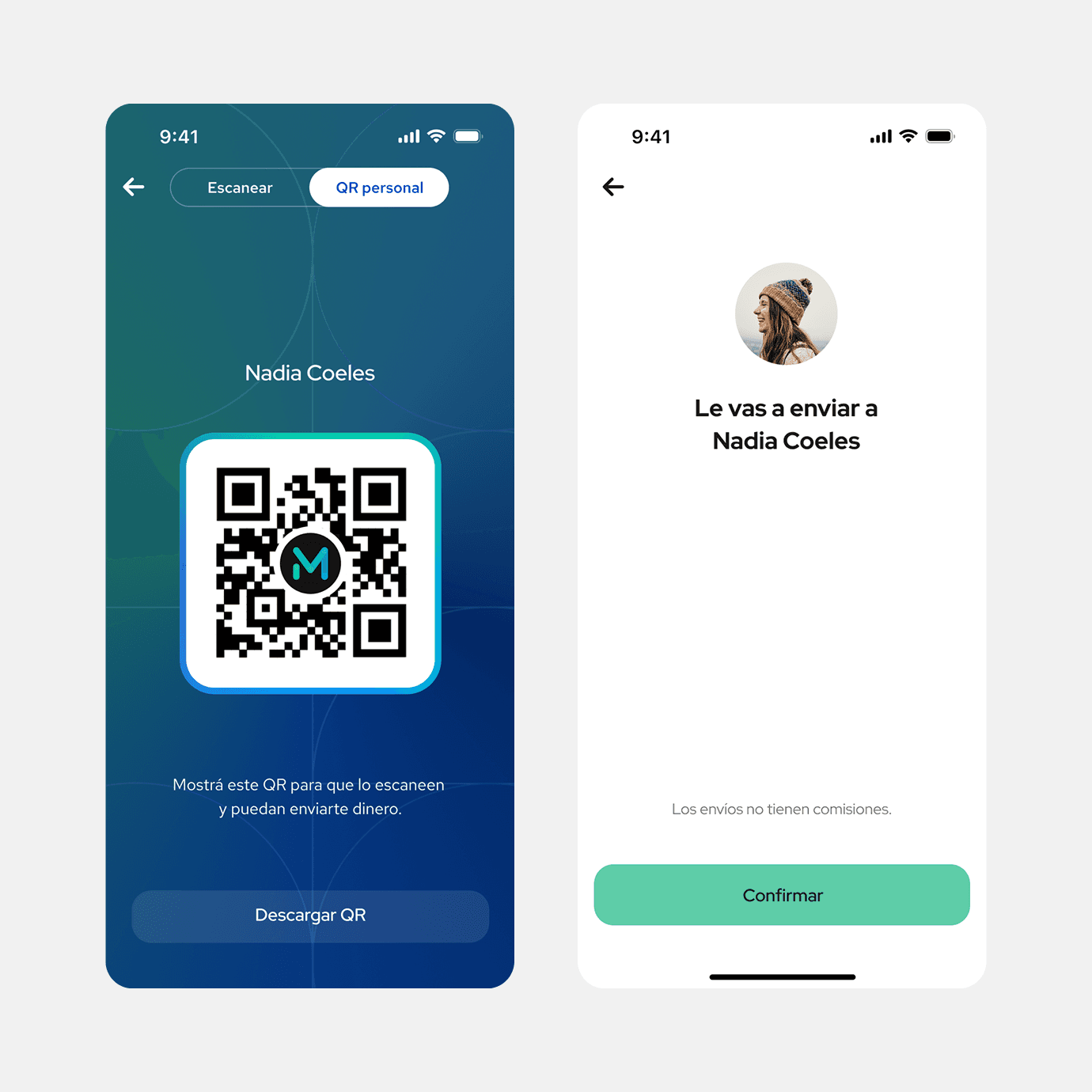

Personal QR Code

Problem

To send money, you needed the other person's phone number. That made spontaneous situations, like splitting a bill with someone you just met, unnecessarily complicated.

What we did

We added a personal QR code each user could show from their profile or the Send flow (Contacts screen). For the MVP we kept it separate from the merchant scanner to avoid a bigger backend commitment, and to prove the hypothesis before justifying the larger investment.

Result

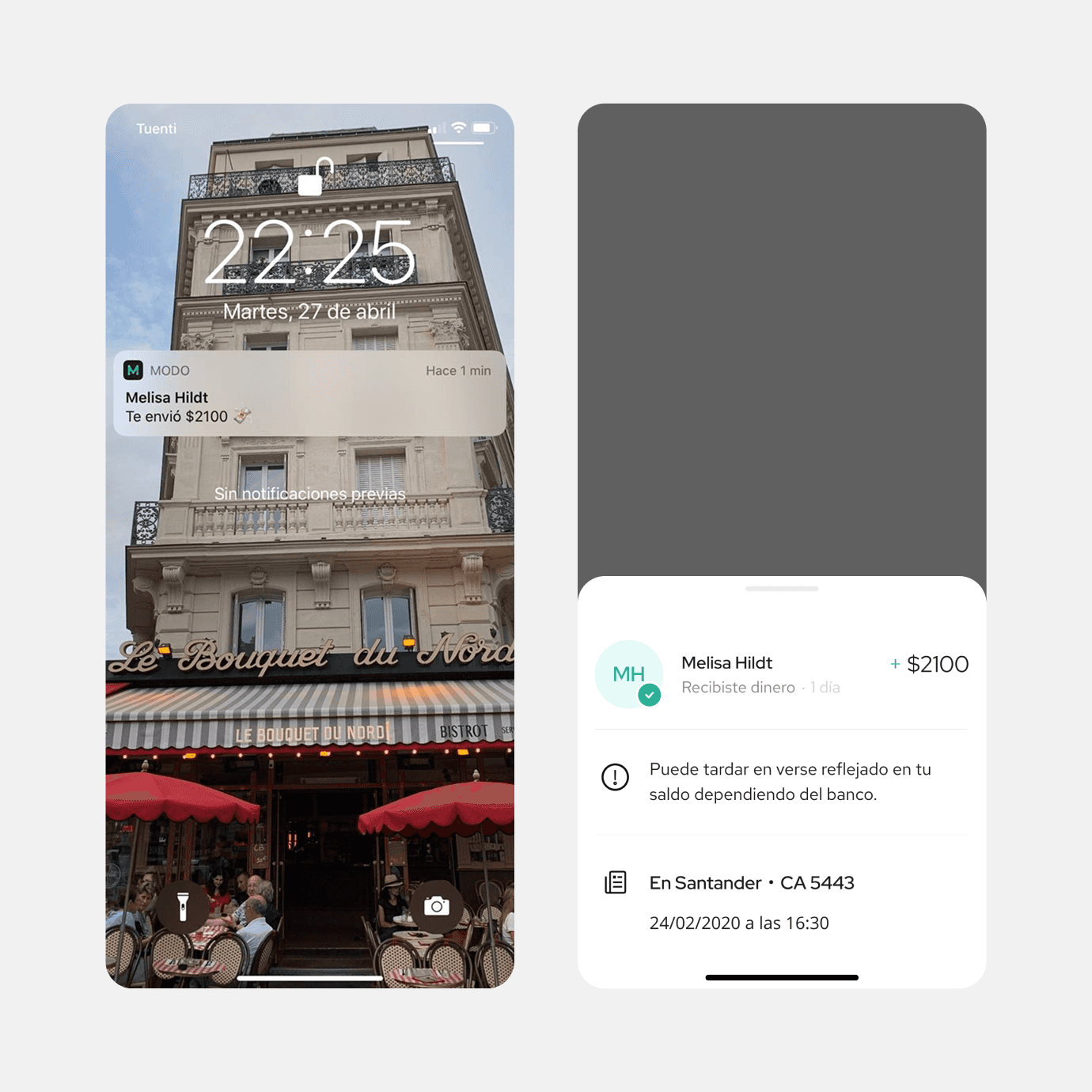

Push Notifications for Received Money

Problem

Most banking apps at the time didn't notify users when they received money. The only way to know was to open the app and check, or wait for a message from the sender.

What we did

We added push notifications for received transfers and tracked open rate in the first month to measure interest. After launch, the "notify via WhatsApp" button inside the app got fewer taps, users didn't need to send manual nudges anymore.

Additional note

The tricky part was timing. MODO knew when a transfer was initiated, but not always when it fully settled. We had to write the notification copy carefully to avoid telling someone they received money before it had actually arrived.

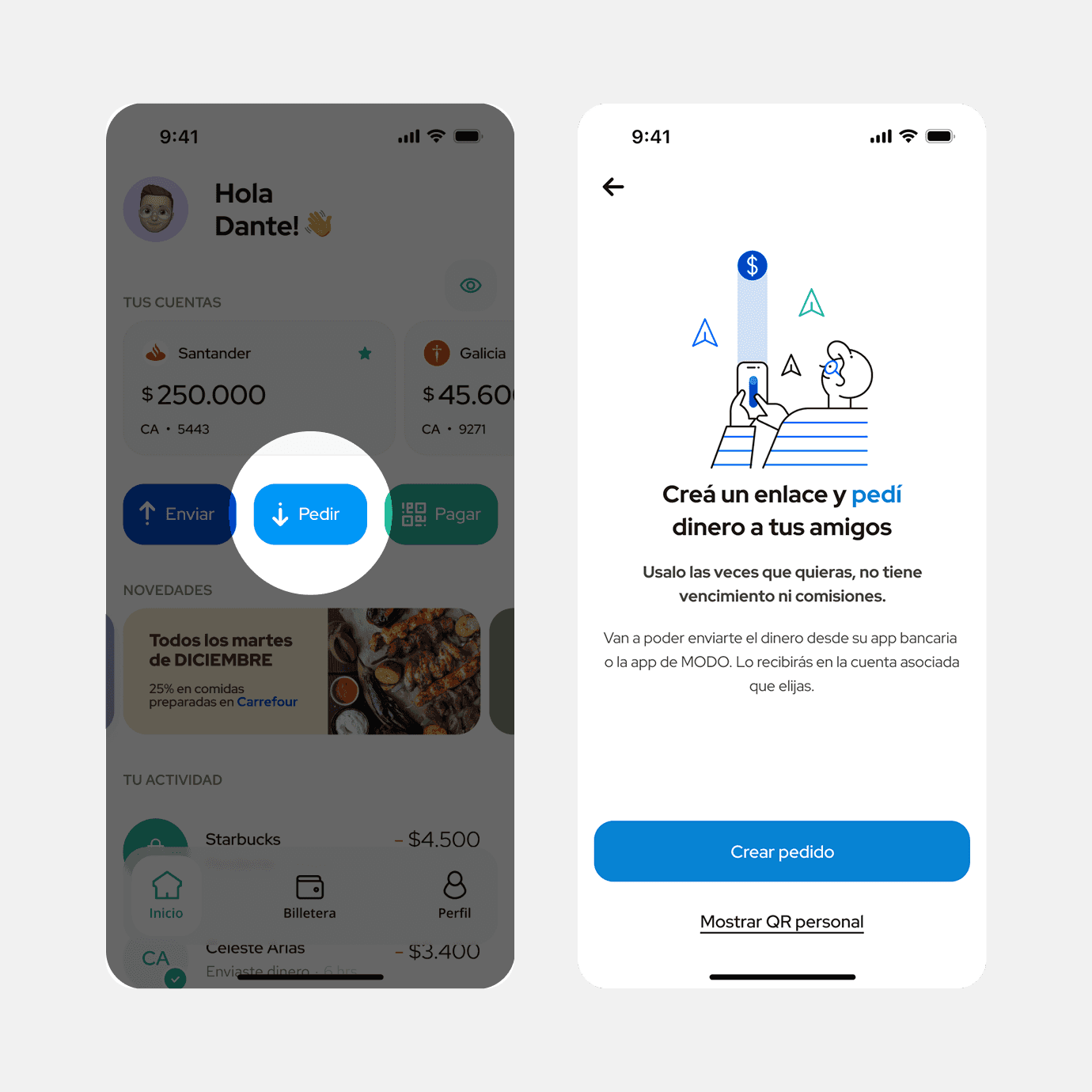

Requesting Money

When language creates the wrong mental model.

Only around 3% of request links were being paid. At first we started discussing missing features, maybe users needed bill splitting, or didn’t understand the value.

Before jumping to solutions, I went into the database to read what people were actually writing in the subject field. Some entries were what you'd expect, splitting rent, paying back a friend. But I kept seeing: "house renovation," "salary advance," "pay my credit card."

People weren't splitting costs. They were trying to take out loans.

The feature was designed to feel casual, pedido de dinero, "money request." But in a banking context, that language sent the wrong signal. I designed an educational screen before the amount step, reinforcing that this was for requesting money from friends, not applying for credit. It also laid the groundwork for adding new features to the flow down the line.

This learning it was a good reminder to look at the actual data before assuming you know the problem, especially since some of those features lived in other bank apps.